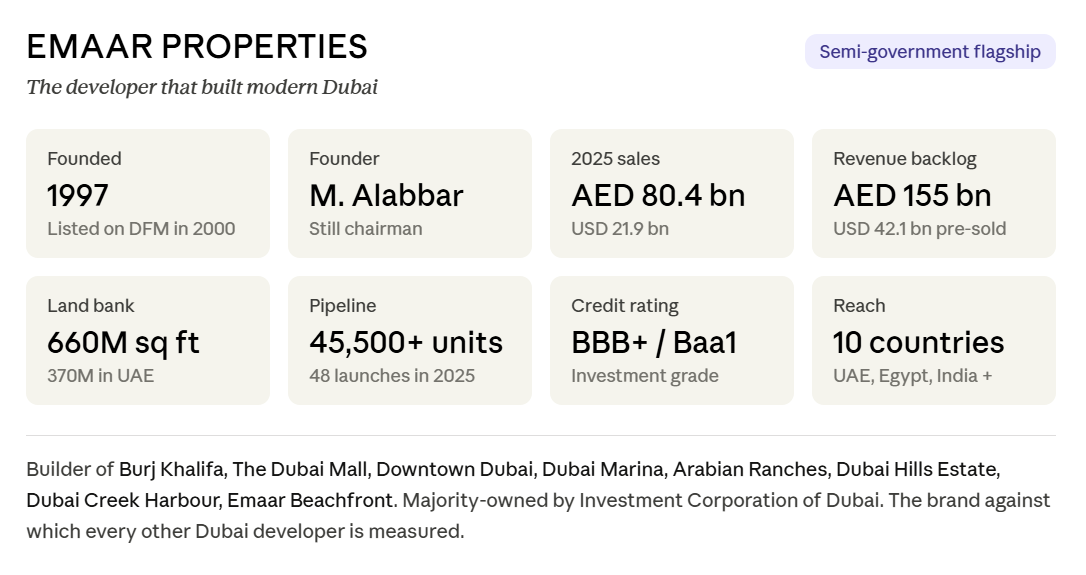

THE DEVELOPER THAT BUILT MODERN DUBAI

Emaar Properties is not just one of Dubai’s developers — it is the company whose buildings define the city’s skyline in international perception. Burj Khalifa, Dubai Mall, Downtown Dubai, Dubai Marina, Dubai Hills Estate, Arabian Ranches, Dubai Creek Harbour, Emaar Beachfront — these are not separate projects. They are a single, coordinated empire built by one company over almost three decades. When a foreign buyer sees a photo of Dubai, they are almost always looking at Emaar.

Founded in 1997 by Mohamed Alabbar and listed on the Dubai Financial Market in 2000, Emaar is a public joint stock company in which the Government of Dubai, through Investment Corporation of Dubai, holds a significant minority stake. This semi-government status is the single most important fact about the company for a buyer — it is the reason Emaar is treated by the market as the closest thing Dubai has to a sovereign-backed developer, and the reason its delivery record is structurally different from privately owned competitors.

In 2025, Emaar recorded AED 80.4 billion in property sales, revenue of AED 49.6 billion, net profit of AED 17.6 billion, and a revenue backlog of AED 155 billion — meaning over USD 42 billion in already-sold units waiting to be delivered. Property sales rose 16% year-on-year to Dh80.4 billion, revenue increased 40%, net profit before tax grew 36%, and revenue backlog rose 39% to Dh155 billion. The company holds a UAE land bank of roughly 370 million square feet, which gives it a development runway no other Dubai developer can match.

gulfnews

The single most important fact about Emaar for a buyer in 2026 is that Emaar is not one product — it is a tiered ecosystem. Treating “an Emaar apartment” as one category is the same mistake as treating “an Emaar Beachfront unit” as one category. The brand spans super-prime trophy assets and mass-market townhouses inside the same parent company, and the resale dynamics, rental yields, and buyer profiles differ sharply between tiers.

THE FOUNDER: MOHAMED ALABBAR

The story of Emaar is the story of one man. Mohamed Ali Alabbar was born in Dubai on 8 November 1956 — into a city that was still a fishing and pearling port with a population under 60,000. His father was a fisherman. He grew up watching Dubai exist as something the world had not yet heard of.

Alabbar studied finance and business at Seattle University in the United States, graduating in 1981, and returned to the UAE to begin his career at the Central Bank of the Emirates. He was then appointed founding Director General of the Dubai Department of Economic Development, working directly under Sheikh Mohammed bin Rashid Al Maktoum on the strategy that would transform Dubai from a regional trading post into a global city. This is the most important biographical fact about Alabbar — he was not a developer who happened to get government contracts. He was the architect of Dubai’s economic diversification strategy who then founded the company that would execute the real estate side of that strategy.

On 16 June 1997, Alabbar founded Emaar Properties. The company went public on the Dubai Financial Market in 2000. By 2005, Emaar was the largest real estate company in the Arab world. By 2010, it had built the tallest building on the planet.

Alabbar’s wider business empire today extends far beyond Emaar — he founded Eagle Hills Properties (international developments in Bahrain, Serbia, Morocco), Nshama (mid-market Dubai developer), Americana Group (regional fast-food operator), and Noon.com (regional e-commerce platform launched in 2017 with Saudi Arabia’s Public Investment Fund). He also owns stakes in Yoox Net-a-Porter and various MENA technology funds. He has seven children. He still chairs Emaar.

For a buyer, what matters is this: Alabbar is the closest thing Dubai real estate has to a founder-CEO with a multi-decade track record. He is not a private developer hoping the next launch sells. He is the person who, alongside the ruler, designed the demand environment that makes the launch sell.

HISTORICAL MILESTONES

Emaar’s history is also the history of modern Dubai. The two cannot be separated.

1997 — Emaar Properties founded by Mohamed Alabbar. First major project: Emirates Hills, the gated villa community that established Dubai’s super-prime residential category and remains one of the most expensive postcodes in the city today.

2000 — Listed on Dubai Financial Market (DFM). Government of Dubai retains a significant minority stake through what is now Investment Corporation of Dubai. This is the moment Emaar became “semi-government.”

2002 — UAE introduces freehold ownership for foreigners in designated zones. Emaar’s projects are among the first to benefit. Dubai Marina launches — the largest man-made marina in the world at the time, eventually housing over 200,000 residents. Arabian Ranches launches the same year — the original suburban villa masterplan that defined what “family living in Dubai” looked like for an entire generation.

2004 — Launch of Downtown Dubai, the 500-acre masterplan around what would become Burj Khalifa. At the time, it was the largest single development project on Earth.

2008 — The Dubai Mall opens — the largest shopping mall in the world by total area. Sets the template for Emaar’s “mall-as-anchor” model that every subsequent masterplan would copy.

2008–2009 — Global financial crisis hits Dubai hard. Emaar share price collapses. Several projects pause. The company survives because of its government link and diversification — many private competitors do not. This period defines who Emaar is for the next decade: the developer that did not default.

2010 — Burj Khalifa opens — 828 metres, the tallest building in the world. Still the tallest, sixteen years later. This single building did more to put Dubai on the global map than any marketing campaign in the city’s history.

2013–2014 — Launch of Dubai Hills Estate (joint venture with Meraas) and Dubai Creek Harbour (joint venture with Dubai Holding). These are not just projects — they are the two biggest masterplans of the post-crisis era and the engine of Emaar’s growth into the 2020s.

2017 — Launch of Emaar South masterplan around Al Maktoum International Airport. A long-horizon bet on the second airport and the southern growth corridor.

2018 — Launch of Emaar Beachfront at Dubai Harbour. Emaar’s first ground-up beachfront masterplan and a direct challenge to Palm Jumeirah’s monopoly on premium beachfront.

2021 — Emaar Malls delisted and merged back into Emaar Properties, simplifying the corporate structure.

2022–2025 — Post-pandemic boom. Emaar sales triple from AED 35 billion in 2022 to AED 80.4 billion in 2025.

Backlog grows from under AED 50 billion to AED 155 billion. The company launches 48 new residential projects in 2025 alone, including Grand Polo Club, The Valley, and Bristol at Emaar Beachfront.

FLAGSHIP PROJECTS

The buildings and masterplans that define the brand:

Burj Khalifa (2010) — 828 metres, tallest building in the world. Mixed-use: Armani Hotel, residences, corporate suites, observation decks. The single most photographed building of the 21st century.

The Dubai Mall (2008) — 1.1 million square metres. Over 100 million visitors per year. Anchors Downtown Dubai and underwrites the surface rents of every Emaar retail asset in the city.

Downtown Dubai — 500-acre masterplan. Contains Burj Khalifa, Dubai Mall, Dubai Opera, and the Address-branded residential towers. The most expensive square kilometre of real estate in the UAE.

Dubai Marina — opened 2003 onwards. The largest man-made marina in the world. Over 200 high-rise towers. Defined Dubai’s image of skyscraper-lined waterfront living.

Arabian Ranches (2002, with Phase II and III through the 2010s) — original suburban villa masterplan. Still one of the strongest resale markets in the family-villa segment.

Emirates Hills (1999) — Dubai’s “Beverly Hills.” Custom-built mansions, Montgomerie Golf Course, the highest per-square-foot land prices in the city.

Dubai Hills Estate (2013, JV with Meraas) — 11 million square metre masterplan, 18-hole championship golf course, Dubai Hills Mall, multiple sub-communities. The dominant family-luxury masterplan of the 2020s.

Dubai Creek Harbour (2013, JV with Dubai Holding) — 6 square kilometre waterfront masterplan along Dubai Creek. Includes the future Dubai Creek Tower (designed to exceed Burj Khalifa). Long-horizon project — handovers running through the 2030s.

Emaar Beachfront (2018) — private peninsula at Dubai Harbour. 27 towers planned, ~10,000 units, 1.5 km of private beach.

Emaar South (2017) — masterplan around Al Maktoum International Airport. Lower price point, longer-horizon bet on the southern corridor and the second airport.

The Valley (2019) — Emaar’s masterplan along Dubai-Al Ain Road. Targeted at end-user families, mid-premium townhouses and villas.

Grand Polo Club and Resort (2025 launch) — newest super-prime masterplan, equestrian theme, top of the current launch wave.

Address Hotels & Resorts / Vida Hotels / Armani Hotel — hospitality arm. Address is the in-house premium hotel brand. Armani Hotel inside Burj Khalifa was the world’s first Armani-branded hotel. This is the foundation of the “branded residences” category that now dominates Dubai marketing.

THE TIERS: EMAAR IS NOT ONE PRODUCT

A common mistake buyers make is comparing prices “from Emaar” without specifying which sub-brand. Emaar operates several distinct development lines, each with its own pricing logic, target buyer, and resale behaviour.

Emaar Properties (flagship) — the original brand. Downtown Dubai, Dubai Marina, Emaar Beachfront, Dubai Hills Estate, Dubai Creek Harbour. Premium pricing, established resale liquidity, the bulk of the company’s brand equity. This is what most foreign buyers mean when they say “I want Emaar.”

Emaar South — masterplan around Al Maktoum International Airport / Expo City. Lower price point, longer-horizon bet on the second airport and the southern growth corridor. Different buyer — usually end-user or patient capital, not flippers.

Emaar Development PJSC — the build-to-sell subsidiary, separately listed on DFM. This is the entity that books most of the off-plan sales. Reported USD 19.4 billion in UAE property sales in 2025 and has over 45,500 residential units under development as of mid-2025. When agents talk about Emaar’s delivery pipeline, this is the engine.

Emaar Misr / Emaar India / Emaar Turkey — international arms. Not directly relevant for a Dubai buyer but worth knowing exists, because international sales surged 124% in 2025 — a signal Emaar is actively diversifying away from pure Dubai exposure.

Address Residences / Vida Residences / Grand Polo Club / Bristol — branded sub-lines within Emaar masterplans. “Address” is the hotel-branded tier (premium), “Vida” is the lifestyle tier (mid-premium), and recent launches like Grand Polo Club, The Valley, and Bristol at Emaar Beachfront sit at the top end of the new launch wave.

WHY EMAAR PRICING IS DIFFERENT

There are three structural reasons Emaar units price and resell differently from comparable units by other developers:

1. The government link. ICD’s stake means Emaar carries an implicit perception of sovereign backing. Buyers, especially foreign institutional money, price this as lower delivery risk. This shows up as a 10–20% “Emaar premium” on launch prices versus comparable competitor product in similar locations.

2. Credit ratings. Emaar holds BBB (Fitch), Baa1 (Moody’s), BBB+ (S&P) — investment grade. No private Dubai developer comes close. For mortgage lenders and institutional buyers, this matters.

3. Backlog economics. AED 155 billion in pre-sold revenue means Emaar is not capital-constrained on delivery. Smaller developers default or delay when sales slow. Emaar can absorb a soft cycle.

The trade-off is straightforward — you pay more at launch, you wait longer in queues for hot launches, and the resale upside on entry-level Emaar inventory is often lower than on equivalent product from aggressive mid-tier developers (Sobha, Damac, Binghatti) where the launch discount-to-handover spread can be wider.

WHAT THIS MEANS FOR A 2026 BUYER

Emaar is the safest brand in Dubai real estate. That is the whole pitch and the whole problem. Safety is priced in. If a buyer’s primary goal is capital preservation, predictable handover, and rental stability — Emaar is the default answer and the question doesn’t need a long discussion. If the goal is maximum off-plan flip upside in 18–24 months — Emaar is usually not the right product, because the launch-to-handover gain is compressed by the brand premium already baked into the entry price.

The right Emaar conversation with a client is not “Emaar or not Emaar.” It is “which Emaar tier, which masterplan, and ready or off-plan.”

CORNER | WATERFRONT | PIER POINT 1, RASHID YACHTS & MARINA | PREMIUM UNIT | -10% BELOW OP

Rashid Yachts & Marina Sales Pavilion – Emaar, Sales Pavilion - Emaar - Dubai - United Arab EmiratesPresenting a premium 3 bedroom waterfront apartment in Pier Point 1, Rashid...

3BR | corner unit | Damac Seacrest, Chelsea tower | Dubai Maritime City | 11,6% below OP

Chelsea Residences by Damac - Dubai - United Arab EmiratesCorner three bedroom, full sea view, 2,100.80 sq ft in DAMAC Seacrest...

6 BR | Villa | The Palm Crown, Palm Jumeirah | AED 2.7M Below Original Price

The Palm - Jumeirah - Dubai - United Arab EmiratesOff-plan 6-bedroom villa in The Palm Crown by Nakheel, Palm Jumeirah. AED...

4BR+Maid Penthouse Duplex | Harbour Views Tower 1 | Dubai Creek Harbour | AED 2M Below Market

Harbour Views - Dubai Creek Harbour - Dubai - United Arab EmiratesReady and vacant 4-bedroom plus maid's penthouse duplex in Harbour Views Tower...

2BR | Ocean Cove Building 1 | Rashid Yachts & Marina | 12.4% Below Original Price

Ocean cove - Marina Cubes Street - Dubai - United Arab EmiratesOff-plan 2-bedroom apartment in Ocean Cove Building 1, Rashid Yachts & Marina...

Distress | 5BR Villa | Address Villas Hillcrest | Below Original Price | Ready and Vacant

Address Hillcrest Villas - Dubai - United Arab EmiratesReady and vacant 5-bedroom branded villa in Address Villas Hillcrest, Dubai Hills...

Let's get in touch - I reply in 24 hrs