CORE FACTS

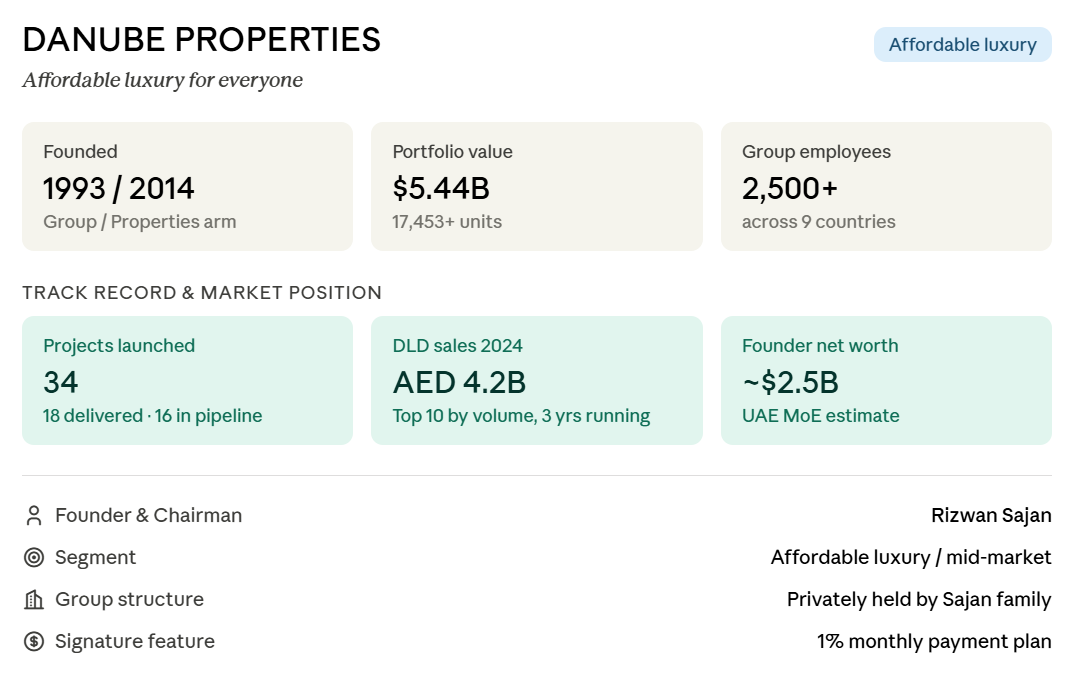

- Founded: 1993 (Danube Group, building materials) / 2014 (Danube Properties division)

- Founder & Chairman: Rizwan Sajan

- Headquarters: Dubai, UAE

- Group employees: 2,500+ across 9 countries

- Portfolio (2025): 17,453+ units valued at $5.44 billion across 34 projects, with 18 delivered and 16 in pipeline

- DLD ranking 2024: Top 10 developers by transaction volume for the third consecutive year, with AED 4.2 billion in registered sales

- Founder net worth (UAE Ministry of Economy estimate): approximately $2.5 billion

- Segment: Affordable luxury / mid-market residential

- Brand philosophy: “Affordable luxury for everyone”

ORIGIN AND BACKGROUND

Danube began in 1993 as a small building materials trading firm in Deira, Dubai, founded by Rizwan Sajan shortly after he moved from Mumbai. The company grew into the GCC’s largest building materials supplier — over 25,000 products under one roof — before launching its real estate division in 2014.

Rizwan Sajan’s personal story is part of the Danube brand. Born in Ghatkopar, Mumbai, he lost his father at 16 and started selling books, firecrackers, and milk to support his family. In 1981 he moved to Kuwait as a trainee salesman, then arrived in Dubai in 1993 with very little. He’s now estimated at around $2.5 billion in net worth and is consistently ranked among the wealthiest Indian expatriates in the UAE.

This origin story matters because Danube Properties is positioned exactly opposite to ultra-luxury brands like Omniyat. Where Omniyat sells exclusivity, Danube sells accessibility — and the founder’s narrative of self-made middle-class roots is a deliberate part of that positioning.

Corporate Structure — Danube Group

Danube Properties is one of many arms of a diversified conglomerate. The wider group operates across 9 countries in the Middle East and Asia, with 2,500+ employees.

DANUBE GROUP DIVISIONS

- Danube Properties — real estate development (the topic of this profile)

- Danube Building Materials — the original business, GCC’s #1 building materials supplier (25,000+ products)

- Danube Home — fastest-growing furniture retail brand across UAE, KSA, Oman, Bahrain, Qatar, Kuwait, India, and Africa

- Alucopanel — the only factory in the UAE manufacturing A2-grade façade cladding panels

- Danube Hospitality — launched 2019

- Danube Sports World — launched 2022

- Filmfare Middle East — media (acquired 2018)

- Cha Cha Chai, Danube Systems — smaller ventures

This structure is the single most important thing to understand about Danube as a developer. Unlike most Dubai developers, Danube doesn’t buy construction materials from third parties — it sources them from its own building materials division. This creates a structural cost advantage of roughly 10-15% on construction inputs, which is what allows the “affordable luxury” pricing to work as a viable business model.

EXECUTIVE LEADERSHIP

Rizwan Sajan — Founder & Chairman, Danube Group

Adel Sajan — Group Managing Director (founder’s son, leads next-generation operations)

Anis Sajan — Vice Chairman, Danube Group (founder’s brother)

This is a family-run business, with succession to the second generation already in motion. There is no institutional board, no sovereign wealth backing, and no public listing — Danube Group is privately held by the Sajan family.

POSITIONING AND DIFERENTIATION

Unique position in the Dubai market:

The 1% payment plan. Danube pioneered the now-famous 1% monthly payment structure: 20% down payment, then 1% per month during construction, with the balance settled at handover (or in some cases, post-handover over 6-8 years). This is the single most recognised feature in Dubai’s mid-market segment, and it earned Rizwan Sajan the nickname “Dubai’s 1% Man.”

Affordable luxury formula. Each apartment comes with: pool on the balcony (in many projects), hotel-style lobby, 40+ amenities (gym, sauna, spa, BBQ, outdoor cinema). The pricing range — AED 450K to AED 1.2M for studios and 1-bedrooms — is dramatically below traditional luxury, while the amenity package is comparable. This is a deliberate gap-filler positioning that few developers have replicated successfully.

Vertical integration via Danube Group. Building materials, furniture, and façade panels are all supplied in-house. This is a structural cost advantage that no other Dubai developer of this size has.

Delivery track record. 18 projects delivered out of 34 launched. In 2025, three projects (Pearlz, Gemz, Opalz) were delivered ahead of schedule — relatively rare in Dubai’s off-plan market. This delivery history is the credibility foundation for the entire 1% plan model, because the plan only works if buyers trust the developer will actually finish the building.

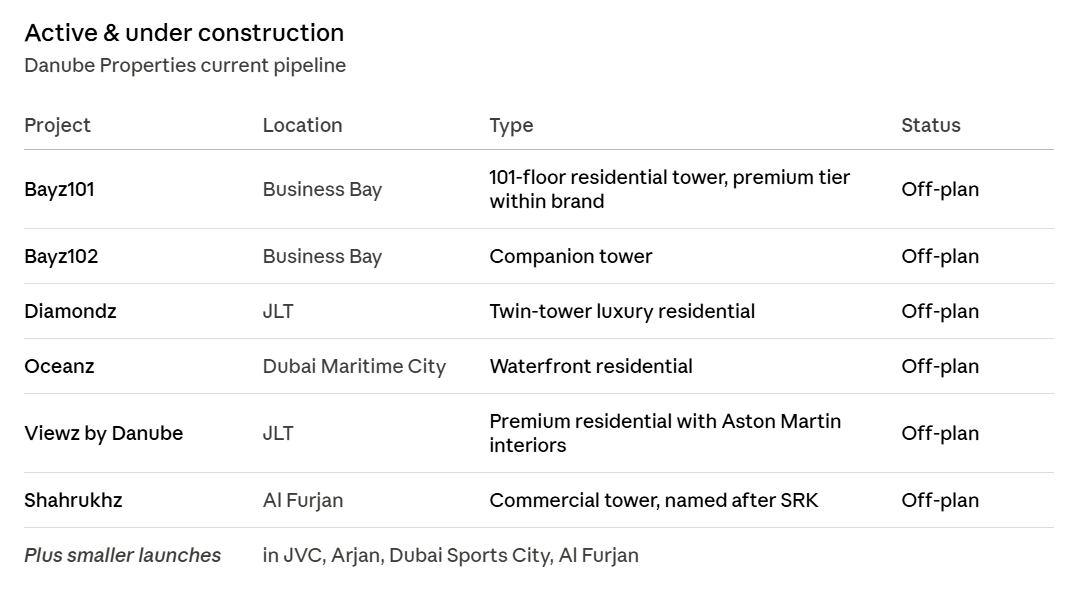

Designer collaborations on interiors. Partnerships with Aston Martin, Tonino Lamborghini Casa, and Fashion TV on branded residences. These collaborations move specific projects above the standard Danube pricing into a premium tier within the brand.

Naming convention. Every Danube project ends in “z” — Glitz, Starz, Glamz, Jewelz, Resortz, Diamondz, Bayz101, Opalz, Pearlz, Gemz, Oceanz, Viewz. The exception is Shahrukhz (commercial tower named after Bollywood superstar Shah Rukh Khan, launched December 2024, sold AED 2.1 billion on launch day).

SIGNATURE PROJECTS

2025 ACTIVITY

In 2025 alone, Danube launched 7 new projects, with 25% of sales attributed to Indian investors — reflecting strong demand from the diaspora and the Sajan family’s network.

Why This Matters for a Broker

Volume play. Danube is high-velocity. Multiple launches per year, fast sell-out, predictable demand cycle. This is one of the easier developers in Dubai to sell rapidly because the buyer pool is broad and the entry tickets are accessible.

The 1% plan is a true differentiator. For first-time buyers and middle-income expats, no other major developer offers a similar structure. This is a real reason to position Danube units to these clients.

Yield positioning. Danube projects in JVC, Arjan, and Dubai Sports City consistently rank among the highest gross rental yield zones in Dubai (often 7-9%). The combination of low entry price + amenity-rich product + high-demand rental zones makes the yield math work.

Delivery track record matters in client conversations. The fact that Pearlz, Gemz, and Opalz delivered ahead of schedule in 2025 is something buyers actually care about, especially after years of delayed handovers from other developers.

Brand recognition is universal in the mid-market. Indian, Pakistani, Filipino, and Egyptian expat communities know Danube by name. This shortens the sales cycle.

NUANCES WORTH KNOWING

The 1% plan has hidden mechanics. While the marketing emphasises 1% per month, in many projects there are bullet payments of 5-8% every 6 months. The effective annual payment burden is typically 22-24%, similar to a standard construction-linked plan.

Buyers need to verify the full payment schedule in the SPA before signing.

Post-handover exposure runs long. Some Danube payment plans extend 6-8 years post-handover. This means buyer financial exposure to Danube as a counterparty continues well after the building is delivered. If a buyer wants to sell during this period, the title is not yet clean — which complicates resale.

Concentrated in mid-market zones. Danube’s footprint is heavily weighted toward JVC, Arjan, Dubai Sports City, Al Furjan, and (more recently) Business Bay and JLT. For clients seeking prime locations like Downtown, Palm Jumeirah, Emirates Hills, or DIFC, Danube doesn’t compete.

Construction quality is mid-market. The amenity package is generous, but the build quality is what you would expect from the price point — not premium. Finishes are functional rather than exceptional. This is appropriate for the segment but should be clearly communicated to clients comparing Danube against Emaar, Sobha, or Meraas.

High-velocity launches create concentration risk. Danube has been launching projects at one of the fastest paces in Dubai. This works as long as the market is strong and new buyer money keeps flowing in. If the market softens significantly, a developer running this kind of cash flow model can face stress. There has been no indication of distress so far, but it’s a structural risk worth being aware of for any buyer with a 6-8 year post-handover exposure.

No institutional backing. Privately held, family-run, no sovereign wealth or bank-syndicated debt structure of the kind that institutionalised players like Emaar or Omniyat now have. This is normal for the segment but means the developer-stability story rests entirely on continued sales velocity.

The “designer collaboration” premium is mostly marketing. Aston Martin interiors and Tonino Lamborghini Casa furnishings raise the price tier, but on resale the brand-collaboration premium often compresses. Buyers paying for these editions should not expect the full collaboration premium to hold at exit